🔥RR #16 Excess of Excesses, CEE Digital Champions, Exploding Seed Market

🔥RR #16 Excess of Excesses, CEE Digital Champions, Exploding Seed Market

Mining for hidden gems in Central Easter Europe

Dear Friends!

As we are nearing the end of the year, it is a good time to reflect on the last 12 months and reaccess the strategy going forward. As I hinted in the last Rounds Review update, I’m slowly adjusting my own course. You should see some changes to the newsletter starting in January/February. I’m planning to announce something new at the beginning of the year so stay tuned.

In the theme of reflection and reassessment, I would like to pull up a quote from a great post from 2016 by Fred Wilson, where Fred discussed how he handles a change in views.

My personal style is “strong views weakly held.” I didn’t come up with that term. My friend Jeremy introduced the concept to me. But it describes me accurately. When an investment opportunity is surfaced, I will immediately have an opinion and I will voice it, often strongly. My colleagues understand that is my style and don’t let me bully the conversation. Because they also know I will fold quickly when the facts prove I am wrong. And I don’t require too many facts to prove that to myself.

As professional investors we constantly take views. Be it a new trend, a new investment or a follow on round. Every time we take a view on something it sets us on a specific course. For me personally, it was B2B Software and the digitization of all business processes. 10 years ago I took the view, that businesses (SMB to Enterprise) will adopt cloud-based software on a massive scale. Anyone following the cloud space will probably agree that I was spot on with my long term view. In the last decade, there were plentiful opportunities to invest in B2B Software across the world. The recent IPO frenzy probably signals the end of that cycle. This made me reflect on my “strong views, weakly held”.

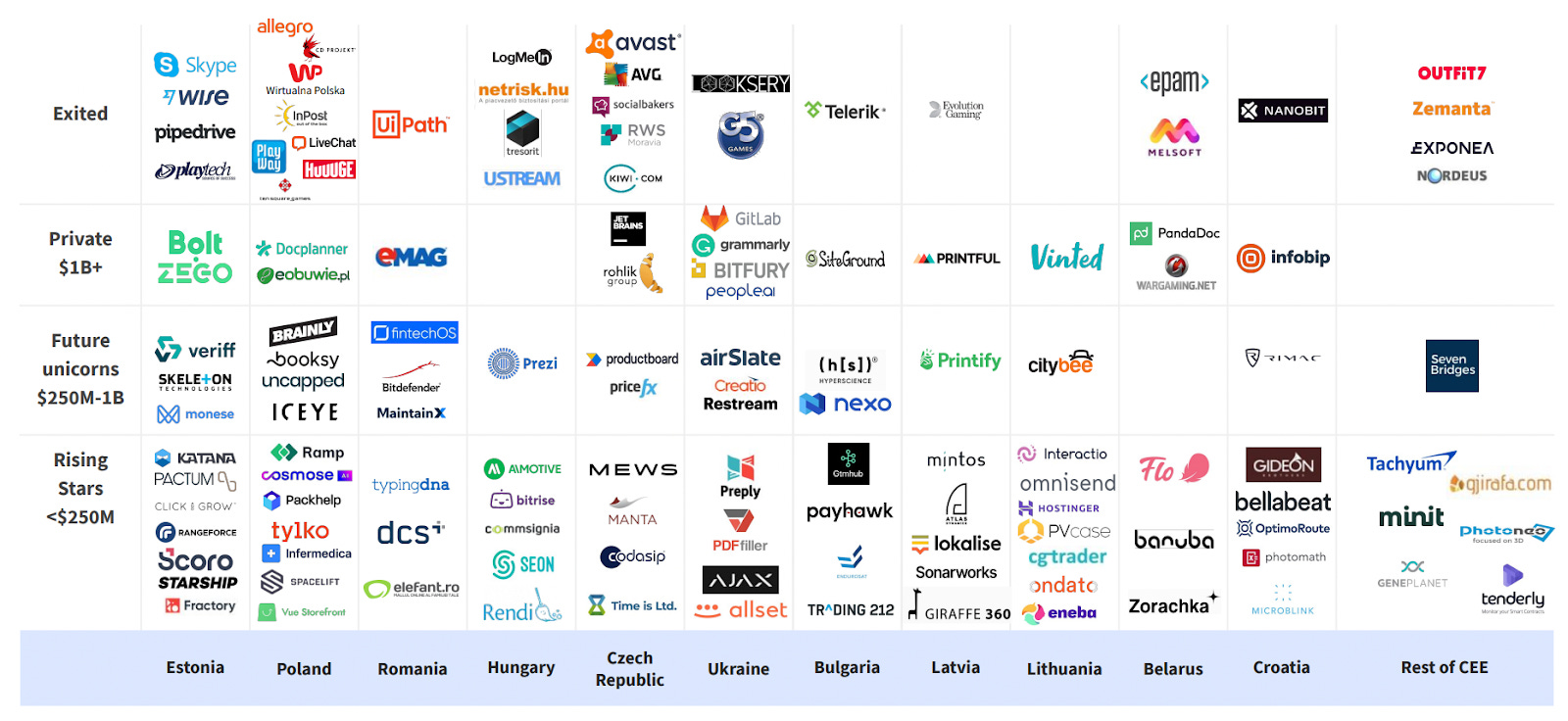

Some of you might have come across a recent Google and Dealroom report on the CEE startup ecosystem. It is an ongoing initiative from Google to map the local tech ecosystem. My friend Joanna Nagadowska is always putting a lot of effort into highlighting the growth of CEE as a tech ecosystem. Below you will find a great overview of where we are right now.

The reason why I focused on this particular slide is that from a B2B Software focused investor point of view, there were plenty of opportunities across CEE to build a top-quartile VC fund with a B2B focused thesis. On the other hand, pure B2B Software is only a subset of all the successful categories growing in CEE. As a pure B2B SaaS investor, you would have to be extremely focused to catch enough of these B2B stars to generate top returns for LPs. Credo Ventures and Earlybird would be my two bets. Inovo Venture (Booksy) and RTA Ventures (Docplanner) would be my other two picks. I would also put Change Ventures in the waiting room (Veriff).

These are some other takeaways from the slide:

as I mentioned in my previous updates - CEE is not a single market. Each country grew its own vibrant tech ecosystem in the last 10 years.

UIPath was an outlier success ($25B market cap), probably will be hard to beat anytime soon

Booksy and Docplanner (both based in PL) are the ultimate “software-enabled” marketplaces originating from CEE. These two companies are unique as both have created marketplaces spanning beyond a single market (hard to do from the region). The only other two companies which come to mind are Vinted and Preply, but they have a strict B2C focus.

Allegro with its recent acquisition of Mall.cz is the undisputed e-commerce leader in CEE. I would assume that is not their final word. There are still two other CEE marketplaces that could provide further consolidation opportunities → eMag and Pigu.

Ecommerce is a rich category in general. Inpost has strongly benefited from the ecomm tailwinds. Their pickup lockers network is probably the largest in Europe. Their mobile app is the most downloaded app in Poland (or one of the most downloaded). Recently, it was suggested that they might become the next Paypal. They definitely have many digital assets they could leverage to build a Chinese-style super app.

Another e-commerce powerhouse, you probably never heard about is CCC (eobuwie, modivo). Based in Poland the group operates some of the fastest-growing e-commerce businesses in the region.

Things are moving fast as my best guess is that Payhawk and Rossum have probably already graduated to the “Future Unicorns” category after their recent rounds.

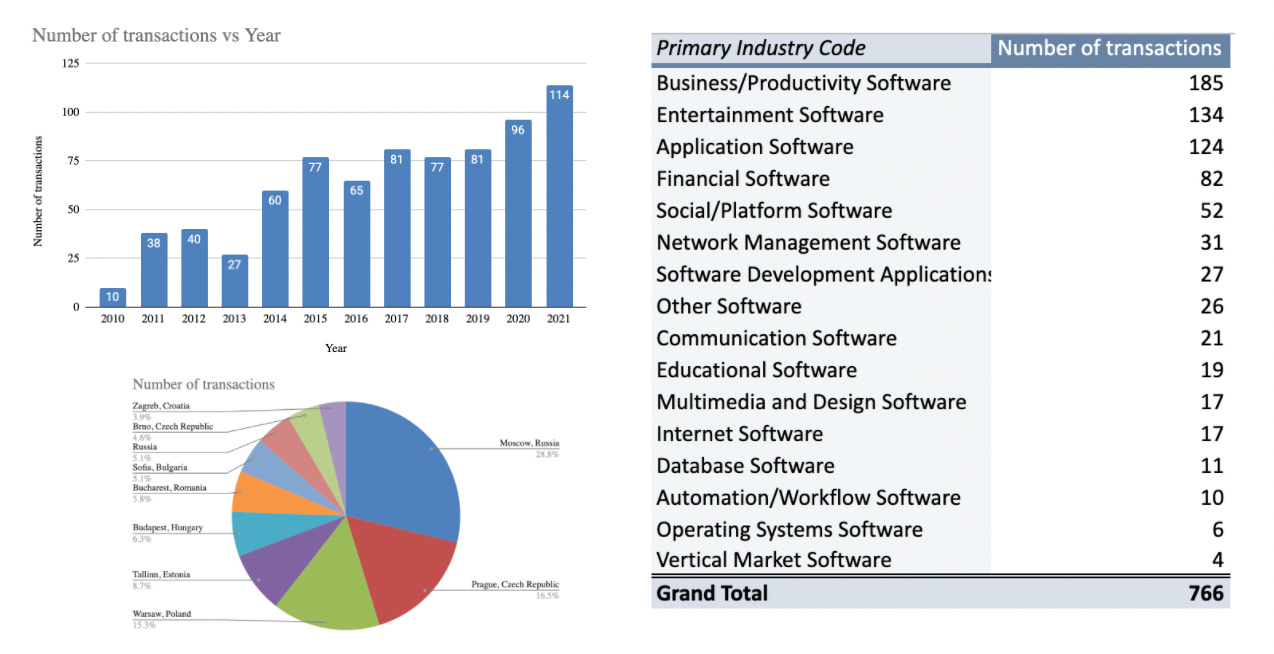

Where does it leave me with my strong views? Well, I continue to believe that CEE will continue to produce great outcomes over the next 10 years. I also believe that local tech ecosystems will get stronger and that local and international competition for deals will increase. I also believe that there will be fewer B2B winners like UIPath, but more winners in new digital realms like blockchain, crypto, metaverse, gaming. I continue to believe that B2B Software will continue to grow in value and significance. What I am not sure about is who will be the best capital allocators in this category. As (cloud) B2B Software matures as a market, maybe we will move from financial capital (VC) to production capital (PE/Strategic) to fund these companies. To back my early thesis I compiled a small data set of the software M&A activity in CEE.

Since 2010, we have seen a 10x growth in the number of software acquisitions in the region. I believe that we are in the early beginnings of this trend. As VC portfolios mature and investors will look to exit their portfolio companies, we should see the number of acquisitions “going up and to the right”. This is my fundamental prediction for the current decade.

If you are interested in this trend, stay tuned as I will unpack more in the coming months.

Lastly, some housekeeping:

I’ve decided, that I will no longer publish the raw data for the announced rounds. Vestbee is doing a great job doing this. You can also subscribe to Dealroom or Crunchbase to pull down the raw data. Inspired by Bartek Pucek (pucek.com) I want to allocate more time to qualitative content.

Instead of publishing the raw data, I will try to put more emphasis on notable rounds. As we are in an outlier type of business, I guess there is only a handful of companies each year that are truly unique.

In future reviews, I will also put more focus on B2B Software, especially Vertical Market Software companies. Headline did a great deep dive on the current VMS disruptors.

Let’s go!

/Marcin

#news and data I've picked up recentlyJosh Wolf of Lux Capital shared another great LP Letter - Excess of Excesses

The VC market is constantly evolving - The Rise of Media-First Investors

Tencent has acquired a majority stake in Bloober Team (PL)

$500M for Seeds - Greylock is disrupting the early-stage game

Pitchbook highlighted an abundance of capital as more money flows into seed

Eleven Ventures raised their third fund, closing at €60M

Panel discussion on the state of the Polish funding ecosystem

Romanian Startup Ecosystem White Paper

#notable rounds🇪🇪 Lingvist raised another €5,1M after their Series A (back in 2015) from Rockaway Capital, Rubio Impact Ventures and MetaPlanet (announcement)

🇸🇰 Enterprise Investors acquired a ~40% stake in Fingo for €19,1M (announcement)

🇨🇿 Rossum raised ~€86M in a Series A funding round (one fo the biggest Series As in the region) from Miton, Seedcamp, LocalGlobe, General Catalyst and Elad Gil (announcement)

🇷🇸 Orgnostic raised a €4,3M Seed Round from Earlybird, Script Capital and a number of notable angels (announcement)

🇨🇿 Resistant AI raised a €14,2M Series A round from Index Ventures, Seedcamp, Credo Ventures, GV

🇧🇬 OfficeRnD raised an €8,6M Series A round from Flashpoint, Runa Capital and Launchub Ventures

🇵🇱 Spacelift raised a €13M Series B round from Insight Venture Partners (first investment in Poland), Blossom Capital, Hoxton Ventures and Inovo Venture Partners

🇵🇱 Vuestorefront raised a €15M Series A round from Creandum (first investment in Poland), Paua Ventures, Earlybird

🇱🇹 PVcase raised a €19M Series A from Elephant, Practica Capital and Contrarian Ventures

#Oct'21 - here is a snippet of the most important numbers📣 44 rounds announced

💰 ~ €287M raised (all rounds converted into EUR)

🚀 One mega-round: Rossum → ~€86M in a Series A funding round

🌍 Creandum, Elephant, Insight Venture Partners, Blossom Capital, Paua Ventures, Localglobe, Seedcamp were among some of the international investors active this month

🇹🇷 Turkey was the most active country (again), 11 rounds raised by companies in Turkey

Few comments based on the data

after a slow September we are back on track with almost €300M raised. Even if we would exclude the Rossum mega-round, it would still be a solid month

I noticed that Poland is starting to attract more international investors. Outside of Vue Storefront, Spacelift, Saleor, Merxu there are a few more companies which should announce interesting rounds soon. It definitely feels like the Polish tech ecosystem is maturing. Estonia and Poland are the two hostpost in CEE tech investing.

This month I noticed that some of the companies moved their HQs outside of CEE. I think this is an ongoing problem with companies trying to look more international and relocating their HQs to the US or UK.

If you’ve found the content interesting, please hit the button below :)

Thank You! You've reached the end of this months update. Much appreciated, I hope you enjoyed the content. If you would like to share feedback or comments feel free to hit the reply button.

PS sorry for all the typos